The Gigawatt Era

AI's new unit of measurement: what one is, what 220 of them by 2030 actually means, and the gap between how often the word gets used and how rarely it gets explained

The word "gigawatt" used to belong to engineers, utility executives, and the occasional Hollywood time-travel movie. Most people did not need to know what one meant, because almost nothing they encountered in daily life was measured in them. A house draws kilowatts. A small factory draws megawatts. Gigawatts were the territory of nuclear reactors and major hydroelectric dams.

That changed quietly, over the past two years. Today, when a hyperscale technology company announces a data center campus, the headline number is increasingly in gigawatts. Meta is building a one-gigawatt campus outside El Paso, with a one-and-a-half-gigawatt site planned for Lebanon, Indiana. Microsoft's Fairwater facility in Wisconsin is approaching the same scale. OpenAI's Stargate talks in tens of gigawatts. The trade press, the financial press, and the policy conversation have all begun using the word as if its meaning is self-evident.

It is not. And the gap between how often it is now invoked and how rarely it is explained matters, because almost every consequential argument about AI infrastructure, from electricity bills to community opposition to whether the buildout is overheating, hinges on what one of these things actually is.

This week's issue is the tour. Not an opinion piece, an explainer. By the end, when you read that some company is building a one-gigawatt or two-gigawatt facility, you will know what is being described: how much electricity it draws, what it occupies on the land, how much it costs, how long it takes to build, and what it produces. And then we will turn to the number that should change how every board, investor, and operator is thinking about the next five years. The world is on track to need not one or two of these. It needs the equivalent of more than 200 of them by 2030.

How Much Power Is a Gigawatt?

A gigawatt is one billion watts, or one thousand megawatts, or one million kilowatts. Those numbers are mathematically precise and intuitively useless. The honest way to answer the question is by comparison.

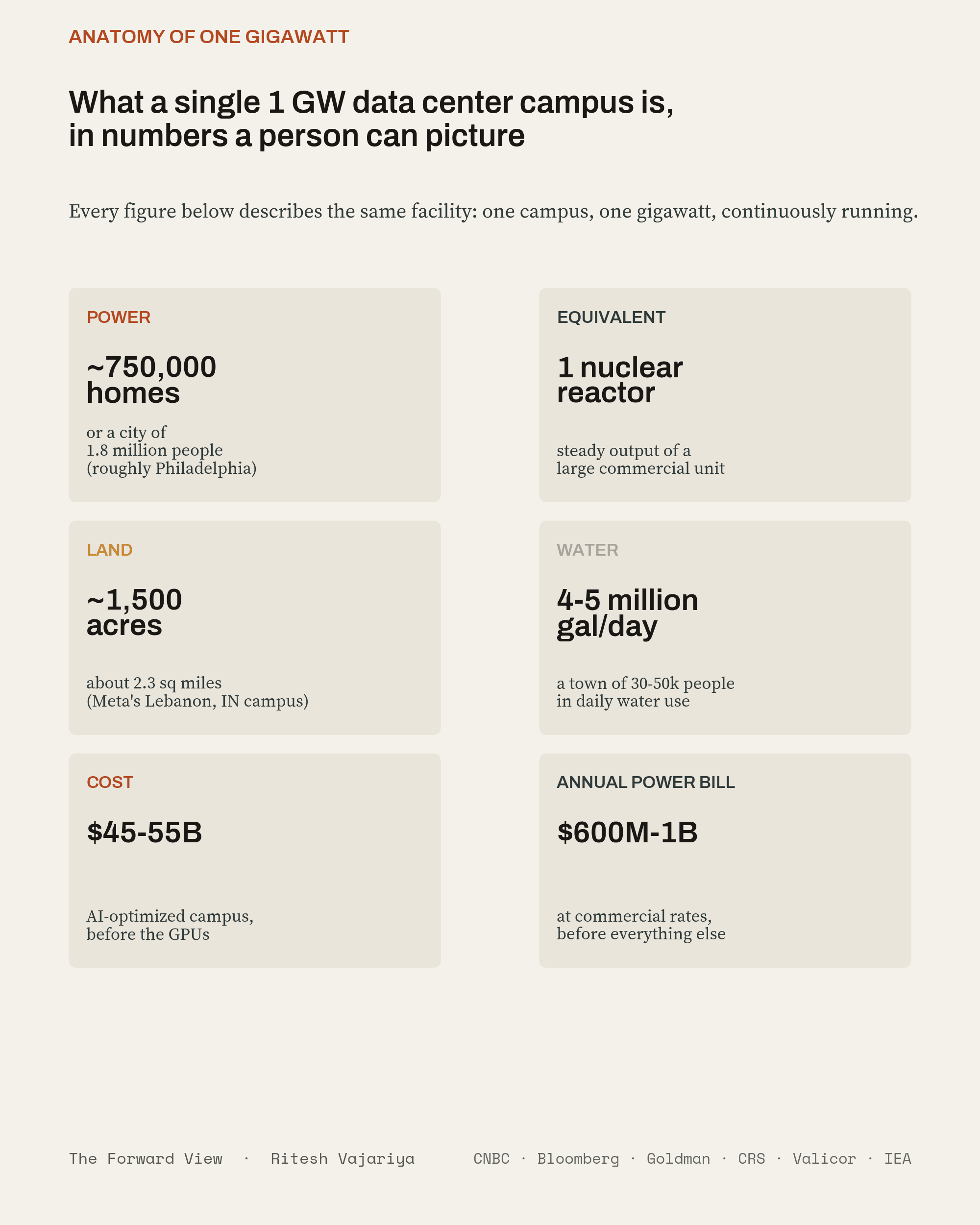

One gigawatt of continuous power is roughly enough to supply electricity to between 700,000 and 800,000 American homes. The range reflects regional differences in household electricity use, but the midpoint, about 750,000 homes, is the figure utility executives use as shorthand. To put that another way, a single one-gigawatt data center campus draws as much electricity as a city of roughly 1.8 million people, comparable in population to Philadelphia or Phoenix.

If you live outside the US, the comparison gets sharper. A one-gigawatt facility running continuously consumes about 8.76 terawatt-hours of electricity per year. That is in the range of a small country's annual demand, depending on which country and which metric you use. The Czech Republic, Greece, and Switzerland all use somewhere around ten times that. Estonia uses noticeably less. The exact ranking matters less than the fact that the comparison is now between a single AI campus and a national power system. The unit of comparison has moved from buildings and towns to countries.

A second comparison, the one Dominion Energy's chief executive used when he told investors that data center developers were asking him for "several gigawatts" of power, is that one gigawatt is roughly the steady output of a large nuclear reactor. Sit with that for a moment. When a tech company announces a multi-gigawatt campus, it is asking the grid to deliver the equivalent of one or more dedicated nuclear power plants, on a timeline of years rather than the decade-plus a new reactor takes to build.

A third comparison gets at scale relative to whole jurisdictions. Running continuously, a one-gigawatt facility consumes about 8.76 terawatt-hours of electricity per year. That is more than the total annual electricity sales in Alaska, Rhode Island, or Vermont. And data centers as a category are now genuinely big inside specific places: in Ireland, data centers consume roughly 21 percent of all national electricity. In Virginia, the world's densest data center market, the share is around 26 percent of state power. These are not projections. They are the current operating reality.

One complication worth flagging before we move on. When companies say "one gigawatt," they may mean different things. Sometimes it is total campus power including cooling and overhead. Sometimes it is the IT load that reaches the racks. Sometimes it is contracted utility capacity. Sometimes it is a long-term buildout target rather than current energized capacity. A campus can be announced as one gigawatt years before all of that power is physically available, permitted, interconnected, and consumed. The comparisons above describe a facility actually running flat-out at one gigawatt, which is the right benchmark to use when reading any announcement, even if the project does not get there for several years.

The Physical Footprint

A modern one-gigawatt campus does not look like a single building. It is a cluster of large, low, rectangular structures spread across hundreds of acres of land, surrounded by substations and transformer yards (the gear that steps high-voltage grid power down to the voltage racks can use), cooling infrastructure, and security fencing.

Meta's recently announced Lebanon, Indiana campus is a useful reference point. It sits on 1,500 acres, slightly more than two square miles, and will consist of thirteen buildings: ten data center halls and three for logistics and administration. The total investment is over ten billion dollars for one gigawatt of capacity.

The buildings themselves are deceptively plain. From the road, a hyperscale data center looks like a giant warehouse: tall, windowless, often one or two stories, clad in metal panels. Inside, the space is dominated by tightly packed rows of server racks, raised floors carrying cabling and chilled air, and overhead distribution systems carrying power. A single building can run hundreds of thousands of square feet. The full one-gigawatt campus easily exceeds several million square feet of enclosed space, more than a dozen large American malls combined, ringed by substations the size of small office buildings, cooling towers, and dozens of diesel generators on concrete pads as backup power.

And then there is water. Most hyperscale facilities use evaporative cooling, the same principle as a swamp cooler at industrial scale: water absorbs heat from the servers, circulates to cooling towers, and a chunk of it evaporates away. The arithmetic works out to 400,000 to 550,000 gallons per day at the 100-megawatt scale, which scales up to four to five-and-a-half million gallons a day for a one-gigawatt site. At the upper end, that is a town of 30,000 to 50,000 people in daily water use. Google's Council Bluffs facility, one of the most compute-intensive in the world, peaks at around 2.7 million gallons per day in summer.

This is the physical thing. Hundreds of acres of land, millions of square feet of building, a substation district at the perimeter, a small reservoir's worth of cooling water moving through the system each day, and enough backup diesel to keep the lights on through a regional blackout.

What It Costs to Build, and What It Costs to Run

The financial scale depends heavily on what you are counting. A standard hyperscale data center costs somewhere between seven and twelve million dollars per megawatt to build just for the site itself. For an AI-optimized facility, with higher rack densities, liquid cooling, and the electrical infrastructure required for large clusters of modern GPUs, the cost can exceed twenty million dollars per megawatt. The civil work, the buildings, the electrical and cooling systems, and the site infrastructure for a one-gigawatt campus run into the ten-to-twenty-billion dollar range before any compute hardware is installed. Meta's El Paso campus and its Lebanon, Indiana campus are each disclosed as one-gigawatt builds at over ten billion dollars, in line with that range.

That is just the building. The GPUs that fill it are bought separately. Once you add the accelerators, the networking, the storage, and the inevitable refresh cycles as Nvidia ships its next generation every twelve to eighteen months, the all-in capital tied to a gigawatt-scale AI campus moves toward far larger numbers. The building is expensive. The power infrastructure is more expensive. The compute that goes inside it can be more expensive still.

Electrical and cooling systems together consume roughly 60 percent of the construction budget. The walls and the roof are a small share. The most important thing to understand about the economics is that a data center is not a building with electrical equipment inside it. It is a piece of electrical and mechanical infrastructure that happens to need a building to shelter it.

Operating costs continue from there. At commercial electricity rates between seven and twelve cents per kilowatt-hour, a one-gigawatt facility running continuously generates an annual power bill between six hundred million and slightly over one billion dollars before any efficiency gains. That is electricity alone, before payroll, maintenance, water, taxes, security, or the depreciation of the hardware inside.

anatomy of one gigawatt

The Time It Takes

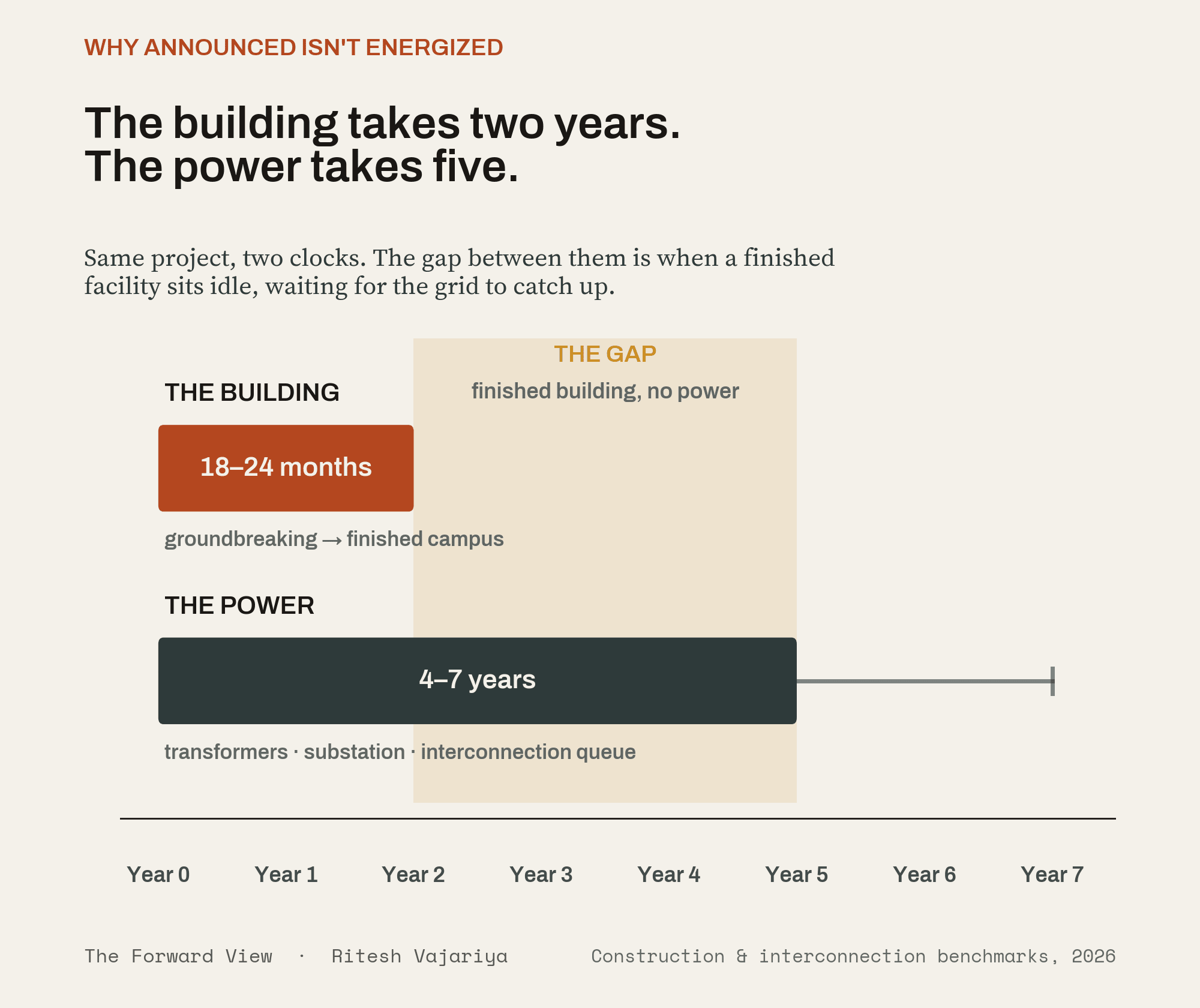

The construction itself is faster than most people assume. A hyperscale data center building, once permits are in hand and the site is prepared, can be built in eighteen to twenty-four months, and some hyperscalers using prefabricated modules have pushed that down further. What takes longer is everything else: the land has to be acquired and zoned, environmental review has to be completed, local planning approvals have to be secured, and increasingly those approvals are contested. The fiber has to be brought in. Most critically, the power has to be brought in, which means a transmission interconnection to the regional grid. In the major data center markets, Northern Virginia, Phoenix, Dallas, the wait just to interconnect a new large load is now running four to seven years. High-voltage transformers, the equipment that physically steps grid voltage down to data center voltage, have lead times stretching to four years and beyond for the largest units.

Here is the strange part. The building takes two years. The power to run it takes five. This is why so many announced gigawatts are not yet running gigawatts, and why several hyperscalers are now building their own power plants on site rather than waiting on the public grid.

build vs power timeline

What a Gigawatt Buys, in Compute

Not all of a gigawatt makes it to the chips. Some of the power runs the cooling, the lighting, the controls, and the building systems. In a modern AI-optimized facility, roughly nine of every ten units of power coming in actually reach the compute. So a one-gigawatt site delivers about 900 megawatts of useful compute power.

Filled with current-generation Nvidia hardware, specifically GB200 NVL72 racks (the top-end AI server platform Nvidia ships today, drawing 140 kilowatts per rack), that 900 megawatts supports roughly 6,500 racks holding around 468,000 individual GPUs. That is enough hardware to train and serve frontier-scale models at a level only a handful of companies and sovereign programs can currently contemplate. The number that matters is not the GPU count. It is what becomes possible when half a million of them sit in one place, connected by the internal networking that only a purpose-built facility can provide. The current frontier of AI capability depends on having clusters of this scale available in single locations. A one-gigawatt facility is, in current terms, the unit of analysis for being competitive at the frontier of AI training and serving. That is why hyperscalers and AI labs are willing to spend the kind of capital they do on a single campus. It is what the frontier currently costs.

The Number That Should Stop the Room

Now multiply.

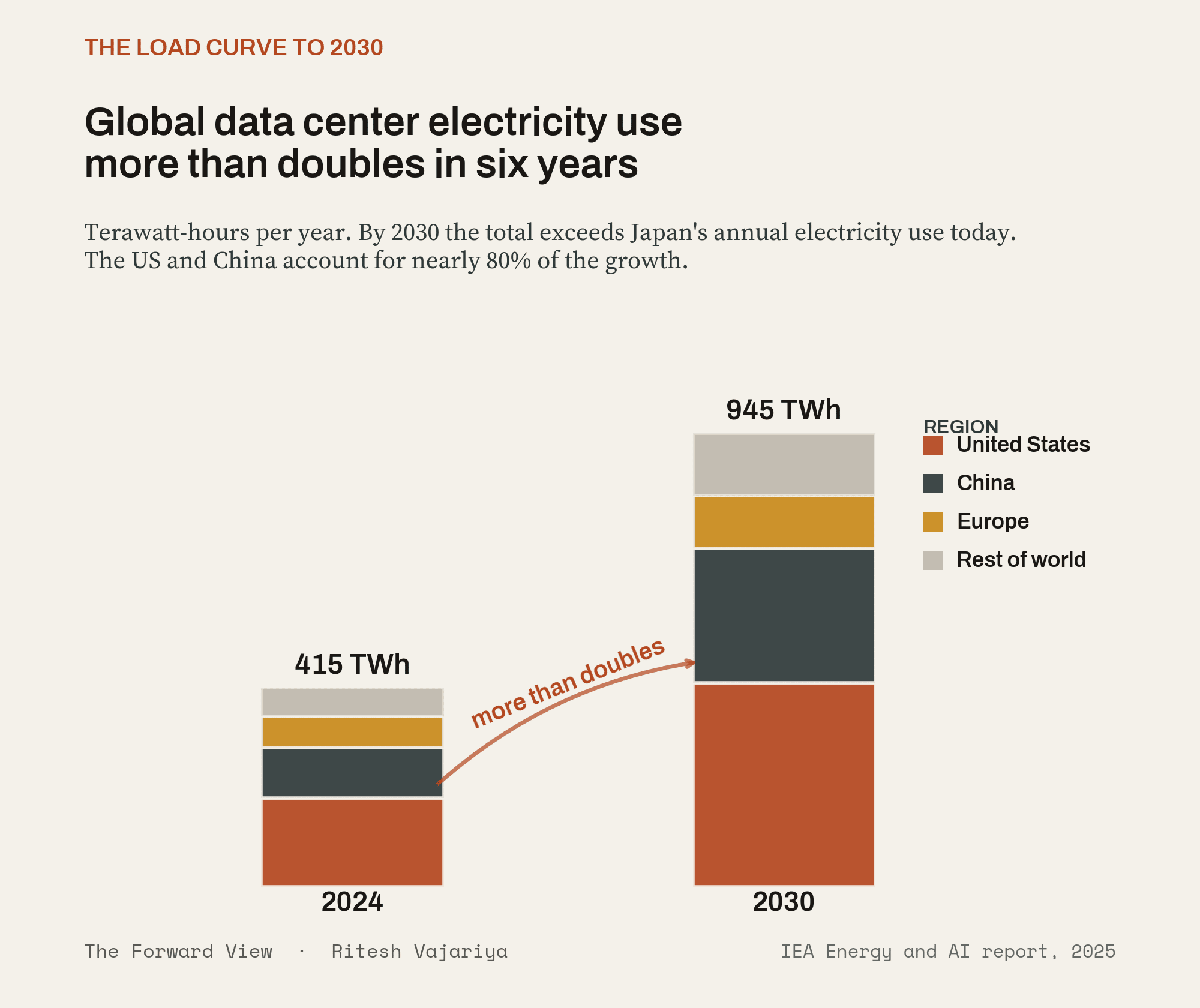

A new McKinsey analysis projects that global data center capacity demand will grow to 219 gigawatts by 2030, with 156 gigawatts of that dedicated to AI workloads alone. The International Energy Agency's parallel modeling puts global data center electricity consumption at 945 terawatt-hours by 2030, more than double the 2024 level and slightly more than Japan's entire annual electricity use today. The US and China together account for nearly 80 percent of that growth.

The actual buildout will not arrive as 219 identical one-gigawatt campuses. It will be a mix of 50-megawatt facilities, 200-megawatt facilities, gigawatt-scale campuses, and a small number of truly enormous multi-gigawatt sites. But the cumulative footprint is the same. By 2030, the world has to bring online a power footprint equivalent to more than 200 nuclear-reactor-sized facilities, occupying hundreds of square miles, drawing as much water as several major cities, costing trillions of dollars, on top of everything that exists today. This is not a "what if" projection from a single research firm. It is the central case across IEA, McKinsey, Goldman Sachs, the US Department of Energy's Lawrence Berkeley National Laboratory, and BloombergNEF. The aggressive end of the range goes higher; the conservative end is still a doubling.

And the timeline does not bend the way capital does. Capital can be raised in months. Permits, transformers, and grid interconnection take years. Skilled construction labor is already short. The political license to build, as last week's issue discussed, has become a national constraint. Every one of those frictions multiplies as the number of projects multiplies. This is the gap that should be sitting at the front of every infrastructure investment committee, every utility long-range plan, and every corporate AI strategy session. The world has decided, more or less collectively, to add a power footprint of more than 200 nuclear reactors' worth of new electrical infrastructure for compute, in less than a decade, using mostly the same supply chains and political systems that took fifteen years to build the last reactor.

global demand by 2030

What This Means in Three Years

The working timeline for most readers is not 2030. It is the next 18 to 36 months. So what changes in that window if these projections hold even partially?

Every major announcement gets read differently. When OpenAI talks about a 10-gigawatt buildout, or a sovereign AI initiative talks about 5 gigawatts, or a hyperscaler talks about adding 2 gigawatts of capacity in a given quarter, the question is no longer "is that a big number?" It is "do they have the substations, transformers, water rights, community approvals, and customer contracts to back that number?" The credibility gap between announcement and delivery becomes the most important diligence question in the sector.

Power becomes a strategic asset, not a procurement item. The operators who locked up firm power, meaning electricity contractually nailed down for years rather than bought on the spot market, are the ones who will still be building at the 2028-2030 horizon. That can mean a dedicated on-site plant, a long-term contract with a specific power generator, or a project sited right next to a utility's plant. And the political economy of AI infrastructure becomes a real risk category. The Permission Problem, the subject of next week's issue, is already producing 300-plus state-level bills in the US alone, with similar dynamics appearing in Ireland, the Netherlands, Singapore, and several Indian states. As the 220-gigawatt buildout unfolds, the geography of where these projects can actually go narrows rather than expanding.

What a Decider Should Do

If you sit on a board, run a portfolio with AI infrastructure exposure, or own a project siting decision, treat "gigawatt" as a technical specification that has to be substantiated, not a marketing number. Ask any operator you are backing what fraction of its announced capacity is energized, what fraction has firm power contracts in place, and what its plan is when those contracts expire or get renegotiated by a new state legislature. And accept that the easy markets are already saturated. The next 200 gigawatts will not all fit in Northern Virginia and Phoenix. Some of it will go to places that do not currently have the grid, water, or workforce to support it, and the projects that succeed there will be the ones that bring those things with them rather than assuming the public infrastructure can absorb the load.

If you advise utilities or regulators, the planning question in front of you has changed. The historical assumption was that electricity demand grows slowly and predictably. That assumption is gone. The grid is now being asked to absorb the equivalent of one or two large nuclear reactors' worth of new load in some service territories (the geographic areas a single utility is responsible for serving) every couple of years, on a timeline shorter than any major capital project the utility has ever delivered. The institutions that adjust to that reality first will set the terms. The ones that do not will be on the wrong end of rate cases (the formal reviews where regulators decide what a utility can charge), political pressure, and customer revolt.

The Bottom Line

A gigawatt is one nuclear reactor's worth of power, one Philadelphia's worth of homes, several thousand acres of land, multiple millions of gallons of water per day, and tens of billions of dollars to build. It supports the kind of compute that makes the current AI frontier possible. And the world has decided to build a footprint equivalent to more than 200 of them by 2030.

When you read in the next press release that a hyperscaler has committed to a two-gigawatt or three-gigawatt campus, the picture should now come quickly. Two cities' worth of electricity. Two nuclear reactors. Several square miles. Tens of billions of dollars for the site, more for what goes inside. And a queue at the substation that may be longer than the building schedule.

We are not entering the gigawatt era. We are already in it. The question is whether the institutions on every side of this buildout, operators, investors, utilities, regulators, and the public, have the right unit of measurement loaded into their thinking. Most do not yet. The next three years will be unforgiving of that mismatch.

P.S. Pick one AI infrastructure announcement that crossed your desk this month. A vendor expansion, a portfolio company commitment, a press release, a policy briefing. Convert its gigawatt number into the comparisons in this issue. Nuclear reactors, cities, water, dollars, years. Then ask the question that follows naturally: does the entity making this announcement actually have all of those things lined up? If the answer is uncertain, you have just found the most important diligence item in your AI infrastructure stack.