Useful Life

The soft spot in the AI capex cycle is not the power line. It is the assumption underneath the earnings.

A few weeks ago, I was in Austin to speak at a private investor briefing. One of the large banks had reserved an entire resort for it. I was there to give the AI infrastructure story, and most of the session covered the usual 2026 material: capacity, power, silicon, buildout timelines.

Then, during Q&A, an investor asked something that sounded like an accounting formality. The hyperscalers carry this hardware on five- and six-year depreciation schedules. Does that match how long the hardware actually lasts?

I didn't have a clean answer in the room. That evening, I did something I hadn't done in a long time. I opened the AWS instance catalog and read it the way I used to when I worked there. The P3 instances were still listed, running NVIDIA V100 chips launched in 2017. So were the G4 instances, on T4 chips from 2018. Nine years on, you can still rent a V100 by the hour. About three dollars, last I checked.

The investor's question assumed the risk was the equipment dying before the books said it would. The instance list says the opposite. The hardware refuses to die. What changed is what anyone will pay to run on it.

Except the price hasn't changed either, not really. A p3.2xlarge still lists at $3.06 an hour. In June 2025, AWS cut prices on its newer GPU families by as much as 45 percent. The V100 wasn't part of that cut. Its price never corrected down to reflect what it's actually worth against a chip three generations newer. It just quietly stopped being anyone's first choice. Nobody repriced it. The market moved on without telling the invoice.

That's the whole piece, really. The most important number in this cycle is measured in years. The years on the books are not the years that matter.

The Numbers Nobody Disputes

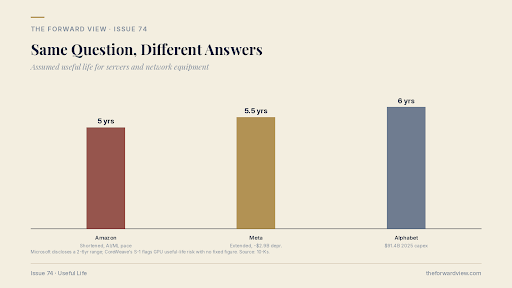

Start with scale, because scale is what makes this matter. Alphabet spent $91.4 billion on capital expenditures in 2025, up from $52.5 billion the year before, most of it on technical infrastructure: servers, network equipment, data centers. With its Q4 results, Alphabet finally put a number on 2026: $175 billion to $185 billion, nearly double again. Microsoft's property and equipment reached $298.6 billion at cost as of June 30, 2025, up from $212.0 billion a year earlier, and depreciation expense climbed with it: $11.0 billion in fiscal 2023, $15.2 billion in fiscal 2024, $22.0 billion in fiscal 2025. Both companies depreciate their server fleets somewhere in a five-to-six-year window. Alphabet fixes it at six. Microsoft's policy gives computer equipment a range of two to six years, wide enough to tell you less than it should.

None of that is where the story is. The story is what happened when two of these companies looked at the same technology cycle and reached opposite conclusions about how long it lasts.

In January 2025, Meta finished an assessment of its servers and network assets and extended their useful life to five and a half years. Based on equipment already in service, it expected the change to cut 2025 depreciation expense by about $2.9 billion. Longer calendar, higher near-term earnings, no new product required.

Effective the same month, Amazon went the other way. It shortened the useful life of a subset of its own servers and networking equipment from six years back to five, citing, in its own words, an increased pace of technology development, particularly in the area of artificial intelligence and machine learning. It expected this to cost about $0.7 billion in 2025 operating income, plus another $0.6 billion from equipment it had already decided to retire early.

Same month, same underlying technology. Opposite conclusions.

None of this is hidden, either. Every number here sits in a public filing, reviewed by an auditor, and disclosed in the way the rules require. None of it is in dispute.

Why This Looks Like Noise

The standard reading treats all of this as background. Depreciation is non-cash, the argument goes, so a change to it moves optics, not the business. A second version says demand is so far ahead of supply that every GPU built this decade runs at full utilization for years, whatever the schedule says. A third points out that useful-life reviews are routine, and companies reassess estimates all the time.

Each of these holds up on its own terms. Non-cash is a real distinction. Demand genuinely exceeds supply right now. Reviews really do happen every year.

None of that is the point. Non-cash is the delayed recognition of cash already spent, sometimes years earlier. Full utilization at declining yield is not the same thing as full earning power. And an estimate stops being routine once the asset base underneath it approaches half a trillion dollars at a single company.

What The Investor In Austin Was Actually Asking

Two accounting teams, two auditors, the same hyperscaler-scale hardware, and they landed on opposite answers within the same month. The whole debate, compressed into one comparison.

NVIDIA didn't make the question easier. It announced its Vera Rubin platform in March 2026: six new chips, co-designed as a single system, on a cadence NVIDIA itself calls annual. NVIDIA says the rack-scale version delivers up to 10x higher inference throughput per watt than Blackwell, at one-tenth the cost per token. That's a vendor claim, and I'll treat it as one. But even a fraction of that improvement decides which generation of hardware gets the high-margin work and which one gets pushed down the stack.

Disclosure: I hold equity in Cerebras Systems, an AI chip company, from my time working there.

That's the real distinction underneath the investor's question, and it isn't the one he asked. There's physical life: how long the thing runs. There's accounting life: whatever a depreciation policy says, five years, six, whatever the study concluded. And there's economic life: how long the equipment earns the kind of margin that justified building it. A GPU doesn't have to die to depreciate faster. It only has to stop being the best option in the room.

Three things make that gap wider than it looks. Modern AI infrastructure is rack-scale, not chip-scale, GPU, CPU, memory, networking, and cooling co-designed as one unit, so a system gets displaced as a whole, not chip by chip. Custom silicon is absorbing more of the internal workload at every hyperscaler, which shrinks the pool of work left for the older GPU fleet to earn against. And power is scarce enough now that every megawatt spent running yesterday's hardware is a megawatt the newest generation doesn't get. None of these three needs the others to be true. Together, they compound.

Run the arithmetic, and the stakes get concrete fast. A hundred billion dollars of AI infrastructure, depreciated over six years, is roughly $16.7 billion a year of expense. Over three years, it's $33.3 billion.

Annual straight-line depreciation on identical infrastructure. Alphabet's 6-year policy vs. shorter assumed lives.

Nobody has to misbehave for that gap to open. Accounting life and economic life just have to keep drifting apart, the way they already are.

CoreWeave has nowhere to hide from it. Its S-1 says plainly that estimating the useful life of its GPUs and its ability to redeploy them once a contract ends is a risk factor that could materially affect results. A hyperscaler can absorb a useful-life miss inside cloud margins or a retail ad machine. A GPU-native cloud has none of that to lean on.

Assumed useful life for servers and network equipment. Two hyperscalers moved in opposite directions the same month.

I wrote about the gap between announced and energized power capacity in a prior issue, Announced Is Not Energized. This is the same project-finance discipline, one layer down: contracted revenue, financing tenor, useful life, time to energize. In 20,000 Chips, I laid out the silicon cadence this piece assumes. The chips keep arriving on schedule. The open question is how long anyone can afford to keep paying for last year's version.

What This Means By 2029

Push the timeline out to 2029. The repricing is already underway in the disclosures, one filing at a time.

Expect more useful-life shortenings to follow Amazon's, not because the hardware is failing but because the cadence Amazon cited in its own filing keeps getting faster, not slower. Expect ROIC to compress across the sector as capital bases outgrow operating income, even at companies that never touch a useful-life assumption. And expect a split between two kinds of operators: the ones who manage fleets on what the hardware actually earns, and the ones who manage on what the depreciation schedule permits. The first group compounds. The second gets repriced, and not gently, once replacement capex stops being a cycle and becomes a permanent line on the income statement.

What A Decider Should Do

If you sit on a board, especially the audit committee, ask management what useful life is assumed for AI accelerators specifically, apart from general-purpose servers and buildings, and what evidence supports five or six years in a market moving on an annual cadence. That is the question this issue exists to put in your hands.

If you run a PE portfolio, make every investment memo on AI compute name three different years, not one: the year the equipment stops running, the year the depreciation schedule stops counting it, and the year it stops earning its keep. A memo that cannot tell those years apart is arithmetic dressed up as underwriting.

If you are a CTO or an infrastructure buyer, model your compute commitments against the vendor's fleet age, not just the quoted price. Ask what happens to your pricing the day the vendor's older fleet gets repriced. It will.

If you advise or invest in this sector, stop grading capex announcements and start reading the property-and-equipment footnote. The construction-in-progress balance and the depreciation start dates already tell you the earnings drag headed your way, months before it shows up in a headline number.

The Bottom Line

The market has spent this cycle arguing about gigawatts and GPUs. The earnings bridge underneath all of it rests on a number measured in years.

Meta added almost three billion dollars to 2025 operating income by adding six months to the calendar. Amazon gave more than a billion of it back by admitting its calendar was wrong. Both moves were legitimate, neither was hidden, and that should worry a board more than either number does on its own.

Accounting life says five years, six years, whatever the study concluded last quarter. Economic life doesn't ask permission. The gap between the two is where the next repricing in this cycle actually starts. It starts in a footnote, not a press release, and it started before anyone in that room in Austin finished asking the question.

P.S. Pick one company you hold, sit on the board of, or compete with. Pull its most recent 10-K. Find the property-and-equipment note. Read the line that gives servers and equipment a useful life, and ask whether anything in that company's own AI narrative actually supports the number of years written there. One filing, one footnote. If the answer makes you uncomfortable, you've found the thing the next few years are going to reprice.